Applying for a mortgage is a major financial decision that can impact your life for years to come. It can be tempting to stretch the truth or withhold information to increase your chances of approval or secure a better interest rate. However, lying on a mortgage application is a serious offense that can result in denial of the loan or even legal consequences. In this article, we will discuss the five crucial things you shouldn't lie about when applying for a mortgage to ensure a smooth and successful loan process.

Unfortunately, though, about 1 in 131 applications contained some form of fraud, according to the 2022 Mortgage Fraud Report from CoreLogic. Industry experts and risk managers are particularly on the lookout for an increase in income fraud risk.

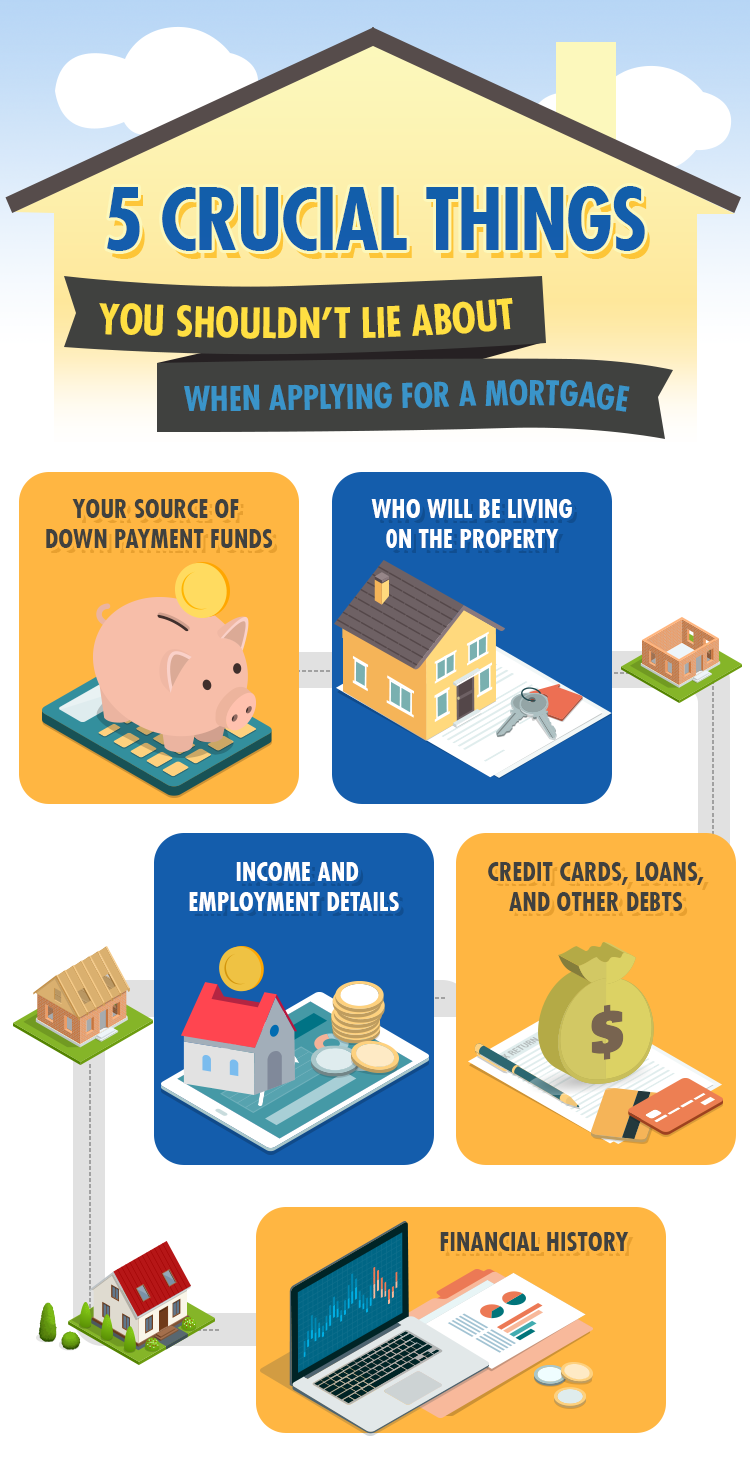

Here we've touched on some of the things borrowers might think it’s okay to lie about during their mortgage application, and why it’s not worth risking your chance to finally buy a home.

Your income and employment status

One of the most important factors that lenders consider when evaluating your mortgage application is your income and employment status. Lying about your income or employment history to increase your chances of approval can result in serious consequences. Lenders will verify your income by reviewing your tax returns, bank statements, and employment verification. Falsifying any of these documents can lead to the denial of the loan and possible legal repercussions.

Your debt and financial obligations

Your debt-to-income ratio is another crucial factor that lenders consider when assessing your mortgage application. It is essential to be honest about your debts and financial obligations to avoid any surprises later in the loan process. If you omit or understate your debt, it could impact your ability to repay the loan, resulting in denial or higher interest rates.

The purpose of the property

It is important to be honest about the intended use of the property when applying for a mortgage. If you plan to use the property as a rental or investment property, you may be required to provide additional documentation and meet different qualification requirements. Misrepresenting the purpose of the property could lead to denial of the loan or even legal consequences.

The down payment amount

The down payment is a crucial part of the mortgage process and can impact your loan approval and interest rates. Lying about the down payment amount can lead to denial of the loan or higher interest rates. It is essential to be honest about your down payment amount to ensure a successful and smooth loan process.

Conclusion

Applying for a mortgage can be a stressful and overwhelming process, but it is important to be honest and transparent throughout the process. Lying on a mortgage application can have serious consequences, including denial of the loan or legal repercussions. By being truthful about your income, debt, property use, credit history, and down payment amount, you can increase your chances of a successful loan process and achieve your dream of homeownership.

The biggest lesson: Just be honest from the start so you’ll have a better chance of getting approved for a mortgage.

FAQs

What are the consequences of lying on a mortgage application?

Lying on a mortgage application can result in denial of the loan, higher interest rates, and legal repercussions.

Can I be approved for a mortgage if I have a low credit score?

It is possible to be approved for a mortgage with a low credit score, but it may result in higher interest rates or additional requirements.

What is the debt-to-income ratio, and why is it important?

The debt-to-income ratio is the ratio of your debt payments to your income. Lenders use this ratio to evaluate your ability to repay the loan.

Can I use a mortgage for